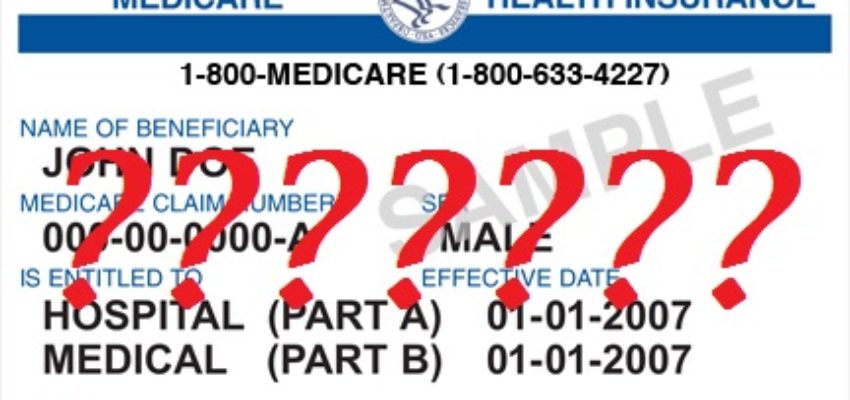

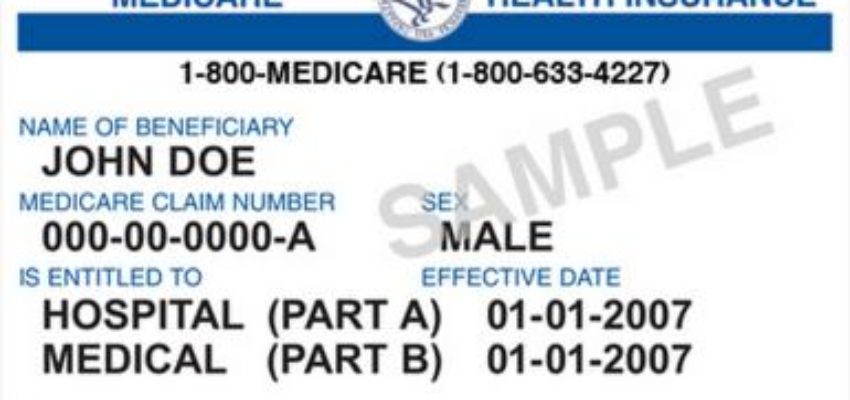

Medicare Employer Information Form

Medicare Part A Coverage –

Are you working and Medicare eligible with insurance either through your own or your spouse’s employer? If this is the case, you should consider taking Medicare Part A (hospital Insurance). In most instances, there is no cost to you for the extra coverage Part A provides. We have included a link at the bottom of the page with the Medicare Employer Information Form. This form helps both you and your employer start your Medicare Part A coverage.

Should you take Medicare Part B coverage?

Before you sign up for Part B coverage there a few things you need to be aware of. First of all, Part B is medical insurance, this coverage is not free and you will be charged a monthly premium. You also need to know; when you are Medicare eligible your employer insurance may change to some extent. Check with your human resources department or benefit coordinator so they can explain any changes in coverage or concerns you have. You will also need to double check insurance information with the Social Security Administration and Medicare.

Health insurance is very important to us all. You don’t want to make mistakes with your healthcare coverage, as that could be costly. Each person has different needs, therefore it is entirely up to you to decide what coverage is best for you. You also have to decide if the costs will be reasonable with regard to your coverage needs.

Primary and Secondary Insurance –

In fact, if you have primary insurance coverage with your employer, most likely you do not need Part B. If you are not satisfied with the coverage your employer provides, you may want to think about Part B coverage. If you choose to add Medicare Part B to your employer insurance you need to find out which insurance will be primary and which one secondary. Primary insurers will pay your approved medical claims first.

Secondary insurance will normally pay the part of your expenses left over after the primary has paid. The amount secondary insurers pay can be either all or some of the unpaid balance. This amount may be the remaining 20% of the doctors fee after primary has paid. If you are not enrolled in a primary insurance plan, but only a secondary plan, you will have little to no coverage. When employer insurance becomes secondary you may be better off if you take Medicare both Parts A and B.

Enrollment Period

Medicare offers a Special Enrollment Period without penalty when you first qualify for coverage. You may enroll in Medicare, without penalty, at any time while you have group health coverage. This enrollment period is also good for eight months after you lose your group health coverage or you (or your spouse) stop working, whichever comes first.

Sometimes your employee coverage will automatically move into a Medicare Advantage Plan (private health plan). If you have health coverage from either a union, a current or a former employer when you become Medicare eligible. You can keep the Medicare Advantage Plan or switch to either Original Medicare or a different Medicare Advantage Plan. You should know that if you switch plans, Your employer or union could lessen or even terminate your health benefits or the benefits of your dependents. Discuss any healthcare plan changes you may want with your employer or union to make sure your coverage is safe.

Click the link below for the employer medicare Forms.

Medicare Savings Program Connecticut

Crowe and Associates wants to help you sort through some of the information on the Medicare Savings Program Connecticut.

Medicare Savings Programs are designed to help Medicare recipients by paying the Part B costs for them. Although Part A is no cost to most people, if the recipient or their spouse has not worked long enough to qualify for this benefit then, the MSPs (Medicare Savings Program), may pay the Part A cost for you. MSP will also pay for the monthly part B premium which everyone pays for. Your income must be within a certain range in order to qualify for the MSP. There are 3 types of Medicare Savings Plans available, each one is based on the recipients income level.

The income limit amounts will remain in effect through March 2018. We have listed the three plans that are available below:

Medicare Savings Program Connecticut: First Plan:

QMB – This plan is for only people who qualify as Medicare Beneficiaries and meet the income criteria as stated below.

Qualified Medicare Beneficiaries (QMB) – There are no asset limits on this plan.

QMB income limits (211% FPL): If you are a single person with income of $2,120.55 or less per month.

If you are a Married couple with income of $2,854.83 or less per month.

This plan pays not only premiums for Medicare Part A and Part B but also deductibles and co-insurances as well. It will also pay for drug plan premium up to the benchmark plan premium, provided coverage in the coverage gap and limit drug copay costs.

Medicare Savings Program Connecticut: Second Plan:

SLMB, this plan is solely for people who meet the following criteria:

SLMB or (Special Low Income Medicare Beneficiary) income limits: (231% FPL) – There are no asset limits on this paln.

If you are a single person with income of $2,321.55 of less per month.

If you are a married couple with income of $3,125.43 or less per month.

This Plan will pay only Medicare Part B premiums. It will also pay for drug plan premium up to the benchmark plan premium, provided coverage in the coverage gap and limit drug copay costs.

Medicare Savings Program Connecticut: Third Plan:

ALMB is also called the Q4. This plan has limited funds, therefore it is only available until the funds are exhausted. This is not an entitlement program and applications can only be accepted while there are funds available. ALMB, (Additional Low-Income Medicare Beneficiary) programs also have no asset limit

ALMB income limits (246% FPL):

If you are a single person with income of $2,72.30 or less per month.

If you are a married couple with income of $3,328.38 of less per month.

This Plan will pay only Medicare Part B premiums. It will also pay for drug plan premium up to the benchmark plan premium, provided coverage in the coverage gap and limit drug copay costs.

TO VIEW QMB vs MEDICADE COVERAGE CLICK HERE

If you would like more information about any of these programs please contact Edward Crowe at Crowe and Associates either by phone at (203)796-5403 or by email at Edward@croweandassociates.com.

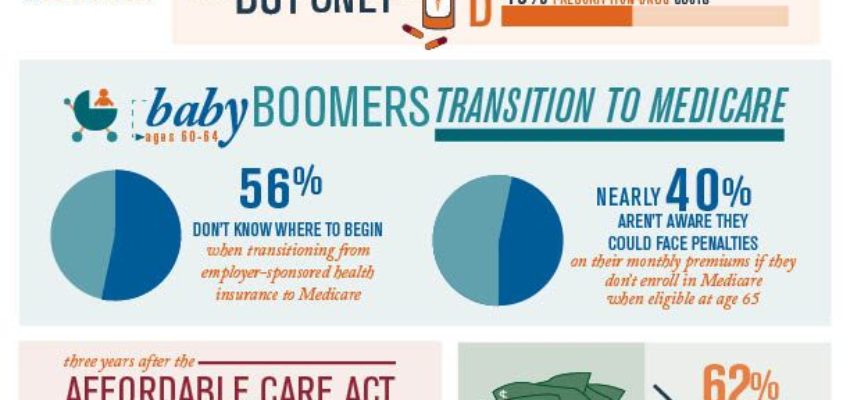

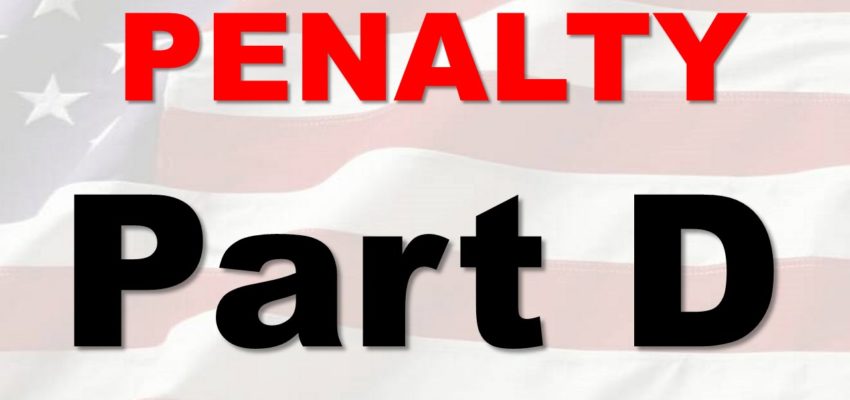

Medicare Part D Enrollment Penalty

How much is the Part D penalty?

The cost of the Medicare part D enrollment penalty depends on how long you go without Medicare Part D or creditable prescription drug coverage.

Medicare calculates the penalty by multiplying 1% of the “national base beneficiary premium” ($35.63 in 2017) by the number of uncovered months you didn’t have Part D or creditable coverage. The monthly premium is rounded to the nearest 10 cents of your Medicare Part D monthly premium. The national base plan premium usually increase each year, so your penalty amount may also increase each year.

Mrs. Jones is now eligible for Medicare, and her Initial Enrollment Period ended on May 31, 2013. She doesn’t have prescription drug coverage from any other credible source. She decided to join a drug plan during the open enrollment period for a 1-1-16 start date. Her drug coverage was effective January 1, 2016.

2016

Since Mrs. Jones was without creditable prescription coverage from June 2013–December 2015, her penalty in 2016 was 31% (1% for each of the 31 months) of $34.10 (the national benchmark premium for 2016) or $10.57. The penalty is rounded to the nearest 10 cents so she would pay $10.60 a month for a penalty. Her current prescription rx plan would include the penalty premium amount with her regular plan premium.

Here’s the math:

.31 (31% penalty) × $34.10 (2016 base beneficiary premium) = $10.57

$10.57 rounded to the nearest $0.10 = $10.60

$10.60 = Mrs Jones monthly late enrollment penalty for 2016

Keep in mind, Mrs. Jones may pay a higher penalty the following year if they raise the benchmark premium for 2017

How do I know if there will be a Medicare part D enrollment penalty?

After you join a Medicare drug plan, the plan will tell you if you owe a penalty and what your premium will be. Most people will have to pay this penalty for as long as you have a Medicare drug plan. The exceptions would be for those that drop coverage or are approved for a drug help program such as MSP.

What if I don’t agree that I have a penalty?

You may be able to ask for a “reconsideration.” Your drug plan will send you a letter explaining how to appeal. All appeals will be sent to a company called Maximus that will review appeals. Maximus is the only company that can review them. As a result, you will need to wait until they make a decision. You must do this within 60 days from the date on the letter telling you that you owe a late enrollment penalty. Also send any documentation that supports your case.

Do I have to pay the penalty even if I think it is wrong?

You must pay the penalty until a decision has been made on the appeal. Failure to pay the penalty could result in termination of your enrollment.

How long does it take to decide on the appeal?

In general, Maximus (Medicare contractor) has 90 days to make a decision.

What happens if Maximus decides the penalty is wrong?

If Maximus decides you should not have a penalty, they will send you a letter stating that fact. Your drug plan will then stop charging you the penalty and will send details regarding a refund of the penalty amount you already paid.

What happens if Maximus decides the penalty is correct?

They will send you a letter stating the penalty is correct. You will be forced to continue paying the penalty if you want to maintain you drug coverage.

Do you have a Medicare supplement plan (also called Medigap)? If so, a high deductible plan F supplement may be a way to save money compared to your current supplement plan. CLICK TO LEARN ABOUT HIGH DEDUCTIBLE F PLAN SUPPLEMENTS

High Deductible Plan F

High Deductible Plan F can save substantial amounts of money on a yearly basis compared to a Medicare supplement plan F, G or N. The following description will detail how the plan works and why it is often a better option for seniors.

What is a high deductible plan F?

A high deductible plan F is a Medicare supplement plan (also called a Medigap plan). It has the same benefits as a standard plan F supplement but with a $2,200 deductible prior to having the coverage of a traditional plan F. Once the deductible is satisfied, the high deductible F covers exactly the same as a plan F. The benefit of the high F is the reduced monthly premium which can be up to 80% lower than the standard plan F premium. Because high F is a standardized supplement, there is no provider network. Medicare supplements do not have networks. You may go to any doctor that accepts Original Medicare.

How does the deductible work?

The high deductible Plan F deductible does not work the same as a traditional high deductible plan. Medicare A and B roughly covers 80% of approved services. The 20% left over is the only amount that goes toward the deductible. The common misconception is the insured needs to pay the first $2,200 of services which is not the case. In fact, most people enrolled in the high F plan do not meet the deductible on an annual basis. The key is to understand what Medicare A and B covers which will provide a better understanding of what charges will go toward the high F deductible.

How much money can be saved on a high F plan?

The savings is in the reduced premium. There is also additional savings when the annual deductible is not met. Premiums vary by state. We will use Connecticut as an example. In Connecticut, one of the lower cost plan F supplements is $239 a month. One of the lowest cost high F plans in Connecticut is $53 a month which creates a substantial savings.

Plan F premium = $239 a month x 12 months = $2,868 annual premium. This premium will be paid regardless of how often the plan is used.

High deductible plan F = $53 a month x 12 months = $636 annual premium. This is a difference in annual premium of $2,232. In the event the full deductible was hit for the year, the total plan cost would be $2,836 ($636 annual premium + $2,200 deductible paid). When the deductible is met, the annual savings is marginal but the deductible is not often met for the year.

How often does the average person meet the $2,200 deductible?

The high deductible plan F works so well because the deductible is not often maxed out. Here are some national averages to consider.

85% of people age 65 to 67 spend $541 a year toward the $2,200 deductible. Remember that Medicare A and B is providing coverage at 80% of Medicare allowable charges and only 20% goes toward the deductible. As a result, this will provide a total annual savings of $1,691 using the high F plan vs. the standard F plan.

80% of people age 68-72 spend $647 a year toward the $2,200 deductible. This would be a savings of $1,585 using the high F vs. the standard F plan

70% of people age 73+ spend $754 a year toward the $2,200 deductible creating a savings of $1,478 a year.

Those that do manage to spend $2,200 for the year will be no worse off than if they had a regular plan F. Maxing the deductible plus the annual premium still has them spending less than the total annual cost for a standard plan F. The benefits are the same once the deductible is met for the year.

What happens if I meet the $2,200 deductible for the year?

If you do meet the $2,200 deductible for the year, your plan will pay all Medicare approved claims. It will work just like a regular plan F. The insurance carrier will track all costs and will pay your claims automatically if you have accumulated costs up to $2,200. Everything is automated, without the need to submit any type of paperwork. Note: Please be sure to use a carrier that provides automatic claims filing. Using a carrier that does not auto file claims may require you to submit paper forms for claims to be paid.

What if I decide I want to go back to my old supplement?

In CT, NY and some other states, you are allowed to change supplements the 1st of any month the entire year. If you try the high deductible plan F and don’t like it, you can change back to your old plan F, G or N any month you like. The change is guaranteed and can not be blocked due to health conditions in guaranteed issue states. The process to change back is quick and simple.

Next steps

Call our office to discuss further at 203-796-5403 or email Edward@croweandassociates.com

CLICK FOR MORE DETAILS ON MEDIGAP HIGH F PLAN

High Deductible Medicare Supplement

High Deductible Medicare Supplement is usually the best option for a Medigap plan if the premium is low enough. The biggest challenge is understanding how the plan works and why it will prove to be a better choice than standard supplements such as F, G and even N.

If you are willing to pay out of pocket for certain health care costs and if your state has a well priced high F plan it could be your best option. A high-deductible Medigap plan F can offer substantial premium savings while still providing dependable coverage. Premiums on high deductible Medicare supplement plan F can run up to 75% less than plan F and G supplements. As with any other supplement, high deductible Medicare supplement plan F still provides access to a huge number of providers because Medicare is still the primary insurance.

How does the High deductible Medicare supplement plan work?

We need to start with an understanding of how high deductible Medicare supplement plan F works. A high-deductible Medicare Supplement Plan F pays the same benefits as a standard medigap Plan F. Its the same only after the insured has satisfied a calendar year deductible. For 2017 the deductible is $2,200. In other words, the $2,200 represents the max out of pocket you pay prior to having full coverage just like a regular plan F.

Out-of-pocket expenses are those expenses not covered by Original Medicare. It is important to keep in mind the deductible is only for the expense that Medicare approves but does not pay all of. The insured does not pay the first $2,2,00 of medical services. You only pay the approved services that Medicare does not pay all of such as deductibles, copays and cost shares.

As an example, assume you have a Medicare eligible expense that costs $5,000 (Medicare approved amount which is usually much less than the provider charges.) Typically, Medicare will cover 80% of the approved charges which in this case is $4,000. This would leave the insured paying $1,000 of the charges. The $1,000 would then be put toward the $2,200 deductible of the high deductible Medicare supplement plan. As a result, there would be a potential to spend $1,200 more out of pocket for the calendar year. If there is another $1,200 of costs, the plan will cover 100% of the remaining Medicare approved services for the year.

Examples of how a high deductible Medicare supplement work using real premiums

Lets use a real example from NY. One of the lower cost high deductible Medicare supplement plans in NY cost $64.00 a month. $64.00 x 12 months is $768 in annual premium. If you max out the $2,200 for the year it will be a total cost of $2,968 for the year. One of the lower cost plan F supplements in NY (example is for the city, boroughs, Westchester county and LI) is $269.50 a month. For 12 months that would total up to $3,234 in annual premium. As you can see, the high F plan will be less even if the full deductible is met.

How much does the average senior spend toward the deductible in a year?

The big savings is when you do not meet the annual deductible. Here are some averages: 85% of seniors age 65 to 67 spend an average of $541 annually toward the deductible. 80% of seniors age 68 to 72 spend an average of $647 annually toward the deductible. 70% of seniors age 73+ spend an average of $754 a year. As a result, the averages favor the person enrolled in the high F plan saving substantial amounts of money every year. If someone does have a bad year and meets the deductible they will still save some money no matter what.

A high-deductible Plan F will almost always provide a savings for those enrolled in it vs. a plan F. The trick is understanding how the plan works. Also, being able to pay any larger sums that may occur early in the policy year. In some states, such as NY and CT, the insured can switch from one supplement to another. They can do this the first of any month throughout the year. Health underwriting is not allowed so you can not be blocked due to health conditions.

How much does Medicare A and B cover and how much will I be left to pay toward my deductible?

Medicare part A is the hospital inpatient part of coverage. There is a deductible for $1,316 for inpatient stays on part A. Part B is 80% coverage after the deductible of $183 (annual). Use the link to see other costs that will accumulate toward the deductible on A and B. Click for A and B benefits and cost share

Do you want to see the premiums for other Medicare supplements such as F,N,G,L and K?

Benefits for supplements in most states are standardized by plan. This means the benefits are the same regardless of which company is offering it. For example, a plan F has the same benefits no matter who offers it. An example of rates is provided. We are using Connecticut Medicare Supplement rates as an example here. CLICK FOR CT MEDICARE SUPPLEMENT RATES

Are you an agent/broker looking to offer a high deductible Medicare Supplement to your clients? CLICK HERE TO LEARN MORE ABOUT HIGH F PLAN SALES

Want a quote for the lowest cost high deductible Medicare Supplement in your state

Call our office to receive a quote over the phone (203-796-5403) or email Edward@croweandassociates.com

Medigap Plans CT

Medigap plans Ct are also called Medicare supplement plans. They provides coverage for these “gaps” in your Medicare coverage and can save you money. Medigap plans are not Medicare Advantage plans rather, they provide coverage after Original Medicare A and B benefits pay. As a result, it is important to note that Medigap plans will only cover services that are approved by Medicare. They will not help cover costs that Medicare does not allow/approve.

Access all Medigap plans CT (Medicare supplement plans) with this link. Site will show you all plans and rates in CT.

Are you a broker looking to sell Medigap plans? If so, click here to learn more about Medigap sales.

Medicare supplemental plans are offered by private insurance companies. These plans help to pay the ‘gap’ between costs covered by original Medicare and your out of pocket costs. Medigap plans are regulated by national and state governments and therefore benefits are generally the same, regardless of the insurance company. For example, Plan A has the same benefits regardless of the company you purchase it from. As a result, rates and value add benefits are the only difference from company to company.

Medigap plans do not cover medication expenses. If you enroll in a Medigap plan, you should also consider a Medicare Part D (prescription drug) plan. The rule is different for drugs under medicare part B. As a result, it is important to pick the right part D drug plan. The pharmacy you like to use and the specific prescriptions you take make all the difference when selecting a drug plan. Call our office to learn more or use the CMS drug plan finder tool.

Want to learn more about the differences between a Medigap plan and a Medicare Advantage plan? Click here to learn about all your medicare options.

We are one of Connecticut’s leading Medicare brokerage firms. Please call us at 203-796-5403 or email us at edward@croweandassociates.com if you have questions. Better yet, we can set a time to sit face to face and discuss all of your options. If you aren’t able to travel to our office, we will gladly come to you.

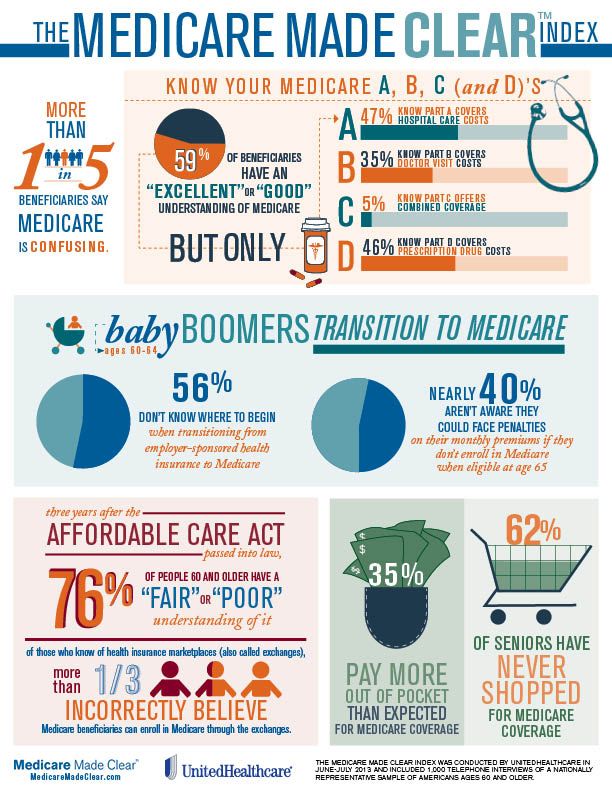

What is Medicare?

This blog will attempt to answer “what is Medicare?” by providing a basic understanding of the Medicare program and how it works. In addition, it will detail the other parts of Medicare such as C and D. First of all lets start with the official definition: Medicare is the federal health insurance program for people who are 65 or older. It is also for certain younger people with disabilities and with End-Stage Renal Disease. Most people are eligible for Medicare at age 65.

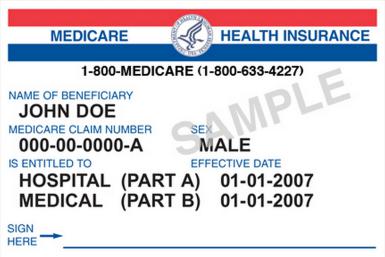

Medicare is made up of four components which can cause confusion. Original Medicare (Red, White and Blue care with a Medicare ID on it) is Medical coverage with parts A and B. This is what provides basic medical coverage for those on the program. Medicare Part C is different than Original Medicare. Part C is a Medicare Advantage Plan and is something a member can enroll in if they want. Medicare Part C replaces Medicare A and B for those that enroll in it. Another part of Medicare is part D which is prescription drug coverage (Also called a PDP). You can enroll in Medicare part D using a stand alone drug plan or access Medicare part D through the drug benefits on an Advantage plan.

Medicare Part A (Hospital Coverage)

Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and also some home health care.

Medicare Part B (Medical Coverage)

Part B covers certain outpatient doctors services, outpatient care, medical supplies, and preventive services.

Medicare Part C (Medicare Advantage Plans)

A type of Medicare health plan offered by a private insurance company that contracts with Medicare to provide you with all your benefits including Part A, B and D. Medicare Advantage Plans include Health Maintenance Organizations, Preferred Provider Organizations, Private Fee-for-Service Plans, Special Needs Plans, and Medicare Medical Savings Account Plans (MSA’s). Therefore, if you’re enrolled in a Medicare Advantage Plan, services are covered by the insurance company/plan and not Medicare because Medicare is not the primary insurance. Most Medicare Advantage Plans offer prescription drug coverage.

Medicare Part D (prescription drug coverage)

Part D adds prescription drug coverage to Original Medicare, some Medicare Cost Plans, some Medicare Private-Fee-for-Service Plans, and Medicare Medical Savings Account Plans. These plans are offered by insurance companies and other private companies approved by Medicare. In addition, Medicare Advantage Plans may also offer prescription drug coverage. They follow the same rules as Medicare Prescription Drug Plans.

What is Medicare: Overall

People often become confused over Medicare. Therefore they confuse Medicare Supplement plans and Medicare Advantage plans with Original Medicare A and B. A Medicare supplement (also called Medigap) is a plan that helps cover the Medical benefits Medicare A and B do not cover entirely. It is secondary to Original Medicare A and B. A Medicare Advantage plan (often called part C) is a plan from a private insurance company. Especially relevant is a person with a Medicare Advantage plan does not use Original Medicare as their insurance. Instead , they use the Advantage plan. As a result, it is not possible to have both plans at the same time.

Medicare Eligibility

Medicare Eligibility is available to anyone turning 65, disabled prior to the age of 65 or with ESRD. People turning age 65 need to have 40 quarters of working credits or have a spouse with 40 quarters. You must also be a U.S resident or be legally in the U.S. for 5 concecutive years. The CMS website has a lot of very detailed information on this topic. Click for CMS details on Medicare A and B enrollment

Steps for Medicare eligible people

- Step 1- It is easy to sign up for Medicare A and B online. CLICK HERE FOR THE SITE TO SIGN UP FOR MEDICARE A AND B . Please note, your Medicare A and B will start on the first of the month you turn 65. Medicare will charge most people $134 a month for part B. They either bill quarterly or draw it out of your Social Security check. (for those taking Social Security)

- Those over the age of 65 can not enroll in A and B online. Please call your local Social Security office to enroll in A and/or B.

- Step 2- Some people do not have to pay the $134 monthly premium. If you are single and make less than $2,435.40 or as a couple make less than $3,284.10 you are eligible for a program called Medicare Savings Program (MSP), Enrolling in MSP will provide a number of benefits and you will no longer need to pay the monthly part B premium of $134 a month. CLICK TO LEARN MORE ABOUT MSP (we can help you with the MSP application)

- Higher income Part B Penalty– People making an annual income over over $85,000 (single) or $170,000 (couple) will pay a higher amount for part B. CLICK HERE FOR INCOME LEVELS

- Step 3- The next step is to figure out which type of plan works for you. There is a lot to choose from including Medicare Advantage plans, Medicare supplement plans (also called Medigap) and/or a Medicare Part D drug plan. There are a number of companies offering these plans. Contact our office to see which plan type is best for you. When a chocie is made, our office will help ensure you are enrolled properly. Applications must be sent in prior to the 1st of the month you turn 65 in order to get the appropriate start date.

Notice about the Part D rx penalty

Currently enrolled in Medicare: Click here to check your enrollment

Medicare Eligibility: Other Resources

Sign up for Medicare after age 65 ( Medicare general enrollment period)

Medicare Part D Rx income penalty

Individual Dental and Vision Insurance Plans

Vision and dental needs are not typically covered by medical insurance plans. Such expenses can total to large amounts during the year. Dental and Vision Insurance plans help to defray the cost of routine care. We offer individual and family dental and vision plans at competitive rates. Both plans have very competitive benefits and national networks.

Dental Plans

Dental insurance plans have access to two different dental benefit designs. Both plan choices use the Ameritus dental network. There is no waiting period for either of the plan types for preventative and basic services. Please note: Preventative and basic services vary by plan. Click here to view a list of services by plan. There is a waiting period for major services. The Choice Dental plan offers a $1,500 annual per person max benefit. The Premier Dental plan offers a $3,000 per person max benefit. Plans both have a $25 per visit co-pay for services. Both plans are available for all ages. Rates are very competitive. Open enrollment rules do not apply. New plans can begin the first of any month.

Hassle free, unassisted online enrollment is available.

Click for dental rates and benefits.

Ready to enroll?

Vision Plan

This vision insurance plan utilizes the VSP vision network. The plan provides coverage for lenses, frames, exams and more. Rates are very competitive. Enrollment can be entered online in just minutes. A link to benefits, rates and provider search has been provided below.

Click here to search for a provider.

Ready to enroll?

Still have questions? Feel free to either call us at 203-796-5403 or email us at edward@croweandassociates.com.

Crowe and Associates is a full service insurance and investment brokerage. Click here to visit our home page.

Connecticut Medicare Plans 2017

The term “Connecticut Medicare Plans 2017” can mean different things. This blog will address the options a person aging into Medicare or already on Medicare will have in Connecticut for 2017. For additional information including signing up for Medicare A and B and rates, you can look at our other blog Medicare Plan Choices Connecticut 2017. We will focus on basic choices for Medicare eligible people in this post. The intent is to provide a general understanding of options available. Look to our other blog if you already know your choices and want more detail. Please email or call us with any questions at 203-796-5403 or email admin@croweandassociates.com.

There are three basic options or types of plans seniors typically use. The Medicare Supplements (also called Medigap) plans, Medicare Advantage plans (also called part C, Managed Medicare or Medicare replacement plans) and finally, there are Medicare part D plans (also called Medicare Rx/drug plans or stand along PDP plans). Medicare Advantage plans (MAPD) include a part D prescription drug benefit. Medicare Supplements (Med Supp) do not have drug coverage so you would need to buy a Medicare part D plan (PDP) if you want drug coverage.

Original Medicare A and B

Connecticut Medicare plans 2017: First things first: In order to enroll in a Medicare Advantage plan or Medicare Supplement plan, you must have Original Medicare A and B. There are rules for eligibility and costs associates with Medicare A and B we will not get into detail about here. Use this link if you want to know the rules for enrolling and costs. Medicare A and B provides medical coverage on its own. It does not provide Rx coverage but does a good job on the medical side. It is feasable to have Medicare A and B only and then a PDP plan for those that want drug coverage. The only flaw with A and B on its own is the lack of an out of pocket max on the benefits.

Other than that, the 20% cost share is not as bad as it sounds due to the Medicare allowable cost amount the providers can bill. This just means Medicare controls how much you are billed for Medical services. Its hard to get a set number but they usually have a discount rate for charges between 50% to 75% depending the service.

Medicare Supplement/Medigap Plans

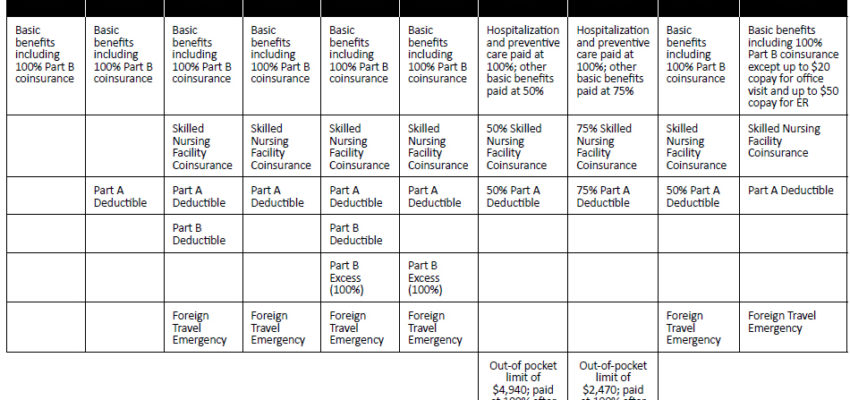

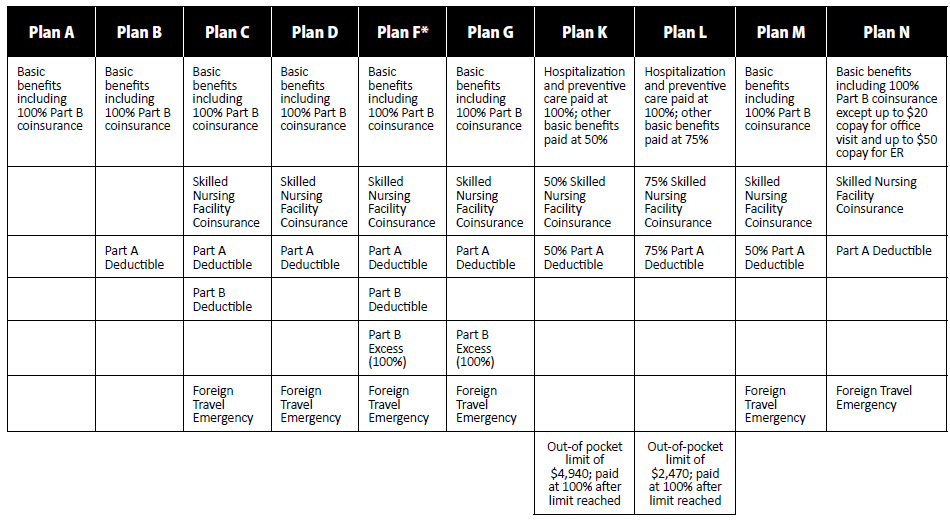

Connecticut Medicare Plans 2017: Many people choose to limit and/or cap the cost share they would pay being on Original Medicare. A Med Supp is a policy that covers some or all of the costs not covered by Medicare A and B. There are 11 different Med Supp plans. Each plan has a letter name that differentiates it from others. Companies offer plans A – N. Not all companies offer all plans. A Med Supp Plan A or B should not be confused with Medicare A and B. They are in no way related. A Med Supp A or B is just two of the 11 supplement options to choose from.

There are a number of plans that are “good deals” in Connecticut. Plans F,N,K, L and High F are available from companies at good prices in CT. Multiple companies offer supplements in CT. United Healthcare is the insurer of the branded supplement plans.

Contrary to the opinion of many,

There are NOT pre-existing condition clauses on Medicare supplements in CT if you have had any type of other coverage in the last 63 days. The only time there are pre existing conditions clauses is if someone did not have any other type of coverage for 63 days and then tries to sign up for a supplement. Some states do allow pre-existing conditions clauses even if there was other coverage in place but Connecticut (and NY for that matter) is not one of them.

The other important thing to note in CT is a person can change from one Medicare Supplement plan to another the first of any month. This is not the case in some states. It is possible in CT. CT is a guaranteed issue state. Also note: If someone is under the age of 65, they do not have access to all the plans. In most cases, clients under the age of 65 are limited to plans A-C.

Medicare Part D Rx Plans (PDP)

Connecticut Medicare plans 2017: PDP plans are stand alone drug plans offered by insurance companies. Medicare does not offer a plan but instead determine what the standard benefit model should look like. Click here for the standard part D benefit parameters. Various companies offer stand alone part D plans including United Healthcare, Aetna, Wellcare, Humana, Envison, Silverscript to mention a few. They all have different benefits and prices but work in a similar manner. Be sure to use a plan that has your drugs in the formulary and also has your pharmacy in network. Some plans will have preferred vs. non preferred pharmacies. It may not be obvious which pharmacies are preferred for your plan. Be sure to use a preferred pharmacy as your copays for the medications will likely be lower there.

Please note: you cannot have a stand alone part D plan and a Medicare Advantage plan at the same time. Enrolling in one will disenroll (kick you out) of the other. The only exception to this is if you have a Medicare Advantage plan called a PFFS plan. They do allow someone to enroll in a PDP at the same time.

Medicare Advantage Plans

A Medicare Advantage Plan, also known as Medicare Part C, Medicare replacement or a Managed Medicare Plan, plans offered by private insurance companies. They often combine medical and drug coverage. While they are not group health plans, they do work in a similar manner. Members pay copays for medical services they recieve. Different services have different copays such as a copay for a primary doctor and a higher copay a specialist doctor. Copays vary from company to company and plan to plan. Most advantage plans offer a part D drug benefit which works similar to a stand alone part D drug plan. Some plans require referrals for specialists while others do not.

Not all HMO plans require referrals but they do require members to stay in network for most services. Advantage plans may cover benefits not covered by Original Medicare and/or a Medicare supplement plan. Benefits and value added services such as dental, vision, Telemedicine, Silver Sneakers , OTC benefits and other programs.

Types of Medicare Advantage Plans

- Health Maintenance Organization (HMO) Plans

- Preferred Provider Organization (PPO) Plans

- Private Fee-for-Service (PFFS) Plans

- Special Needs Plans (SNP)

People are able to change a Medicare plan during Open enrollment. Open enrollment runs from Oct 1 to Dec 7th every year. They can make any changes they want for a Jan 1 start date. Please note: In states that allow underwriting, the member will be subject to medical underwriting if moving to a Medicare Supplement plan. There are additional periods when you can make plan changes such as the MADP, SEP’s and if there is a Trial Right.

Call or email us with any questions regarding this Connecticut Medicare plans 2017 blog. We are able to quote plans options and provide advice at no charge to you. Independent brokers receive commission pay from the insurance companies. You can contact the office either by phone at 203-796-5403 or by email to Edward@croweandassociates.com

Medicare Plan Choices Connecticut 2017

Medicare plan choices connecticut 2017 will cover Medicare Advantage (Also called Managed Medicare or Medicare part C, Medicare Supplments (also called Medigap) and Medicare Part D plans. Various companies in Connecticut offer all three types of plans for 2017. This post will cover all three plan types. Also it will cover how a Medicare receipient can pick the best choice for him/her. Benefit and rate comparisons have been provided below throughout the post. Good luck.

NOTE: There are links below which provide Medicare supplement, Medicare Advantage and PDP plan comparisons for the State of CT. We can run any additional quotes/comparisons that are needed for any product. (MAPD, Medigap, PDP) Call or email our office with any questions (203)-796-5403 or email Edward@croweandassociates.com.

Quick Medicare A and B Information before getting into the plans

First of all, you need to know the basics rules of Medicare A and B. While picking the right plan is important, having Medicare A and B is probably as important. First of all, you must have Medicare A and B to enroll in a Medicare Advantage plan (MAPD) or a Medicare suplement plan (Medigap). A part D drug plan (PDP) requires you to have Medicare part A and/or B. Medicare part A cost nothing for almost everyone while part B costs money every month. CLICK FOR PART B PREMIUMS If you are drawing social security already, the part B premium will be taken out of your check every month. If you are not drawing social security, you will be billed quarterly.

Part A of Medicare covers hospitalization while part B covers outpatient services such as doctors and testing. CLICK FOR MEDICARE A AND B BENEFITS You will see that Medicare covers 80% of Medical costs, as a result, most people want to cover some or all of the other 20%. Finally, it does not cover prescriptions drugs, therefore many people purchase a PDP plan. As a result, those aging into Medicare likely will enrol in a Medicare Advantage plan or a Medigap and/or a PDP plan.

Medicare Plan Choices Connecticut 2017- Medicare Supplements (Medigap Plans)

Medicare Plan Choices Connecticut 2017

A Medicare Supplement Insurance (Medigap) policy, can help pay some of the health care costs that Original Medicare doesn’t cover, like copayments, coinsurance, and deductibles.

Some Medigap policies also offer coverage for services that Original Medicare doesn’t cover, like foreign travel coverage. If you have Original Medicare and you buy a Medigap policy, Medicare will pay its share of the Medicare allowed amounts for covered health care costs. Then the Medigap pays its portion of the cost depending on the plan you have.

A Medigap policy is not a Medicare Advantge Plan.

Things to know about Medigap policies

- You must have Original Medicare A and B

- If you have a Medicare Advantage Plan, you can apply for a Medigap policy, but make sure you can leave the Medicare Advantage Plan before your Medigap policy begins.

- You pay the Medigap premium and the Medicare Part B premium

- A Medigap policy only covers one person. If you and your spouse both want Medigap coverage, you’ll each have to buy separate policies.

- You can buy a Medigap policy from any insurance company that’s licensed in your state to sell one.

- Any standardized Medigap policy is guaranteed renewable even if you have health problems. This means the insurance company can’t cancel your Medigap policy as long as you pay the premium. Furthermore, Connecticut is a guaranteed issue state for Medigap. This allow a change form one Medigap to another throughout the year without any health underwriting.

Medigap policies don’t cover everything

Medigap policies generally don’t cover benefits such as long term care, vision and dental.

Click for Medigap rates Connecticut 2017

Dropping your Medigap and Part D Prescription Drug Coverage:

You have to pay a Part D late enrollment penalty when you join a new Medicare drug plan if:

- Either you drop your entire Medigap policy and the drug coverage wasn’t creditable prescription drug coverage, or

- You go 63 days or more in a row before your new Medicare drug coverage begins

Call or email us with any questions at 203-796-5403 or email Edward@croweandassociates.com. We do not charge a fee for our services.

Medicare Plan Choices Connecticut 2017-Medicare Advantage Plans

Medicare Advantage plans are sometimes referred to as Medicare Part C or Managed Medicare plans . They are Medicare-approved health insurance plans for individuals who are enrolled in Original Medicare, Part A and Part B. When you join a Medicare Advantage plan, you are still in the Medicare program and must continue paying your Part B premium. Original Medicare is not billed while in an Advantage plan, as a result, some people incorrectly think they are not part of the Medicare Program

Medicare Advantage plans provide all of your Medicare Part A (hospital insurance) and Medicare Part B (medical insurance) coverage. Sometimes, they offer additional benefits, such as vision, dental, and hearing, and most include prescription drug coverage. These plans often have networks, which mean you may have to see certain doctors and go to certain hospitals in the plan’s network to get care.

Medicare Advantage plans may potentially save you money vs using a Medigap and PDP plan because the monthly premium is much lower in most cases. Pricing (monthly premium, copays, dedutibles and co-insurance) will vary by plan provider, so it’s worthwhile to compare all plans in your area. Your costs will vary by the services you use and the type of plan you purchase.

Medicare Plan Choices Connectict 2017- Plan options can include:

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Private Fee-for-Service (PFFS) (Not currently available in CT for 2017)

- Special Needs Plans (SNPs)

- HMO Point-of-Service (HMOPOS)

- Medical Savings Account (MSA) (Not currently available in CT for 2017)

You can generally join if you:

live in the service area of the plan you want to join (Most plans in CT are offered in all CT counties with a few exceptions)

- have Original Medicare, Part A and Part B, coverage.

- don’t have end-stage renal disease (permanent kidney failure requiring dialysis or a kidney transplant); however, there are a few exceptions.

Choose your plan carefully. Outside of when you first become eligible to enroll and other personal circumstances that may qualify you for a Special Election Period, you are only able to change plans once a year during the Annual Election Period. The Annual Election Period lasts from October 15 through December 7 of each year. (An exception to this rule is for those that have a “Trial Right” which allows them to change from an advantage plan back to a Medigap and drug plan.

There is also a Medicare Advantage Disenrollment Period, which runs from January 1 through February 14. During this time, individuals enrolled in a Medicare Advantage plan can disenroll from their plan and return to Original Medicare coverage and buy a Medigap and PDP plan if they want to.

One more thing to note is that Medicare Advantage plans, with or without prescription drug coverage, vary depending on where you live. The name of this blog is Medicare plan choices Connecticut 2017. In fact, the rules above apply to most states.

Medicare plan choices Connecticut 2017 – Click Here For 2017 MAPD Plan Comparison CT

Medicare Part D (PDP) Plans CT 2017

A prescription drug plan (PDP) is an option for those eligible that want to enroll in the Medicare Part D prescription drug coverage, which can lower the costs of prescription drugs for insured. A prescription drug plan (PDP) is a stand-alone plan, covering only prescription drugs. Enrollees who choose the option of prescription drug coverage through a Medicare Advantage plan would also have coverage for other medical expenses as part of that plan. Medicare Advantage drug plans and stand alone PDP plans are different but the drug coverage portion works in a similary manner. Enrollees pay a co-pay for each prescription, a monthly premium (not with some advantge plans however) and an annual deductible.

Note: Please call or email our office for a full list of PDP plans available in CT

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Term Life Insurance Without Medical Exam

John Hancock SmartProtect Term with Vitality provides up to $1,000,000 of term life insurance with a medical exam. There are a number of companies that offer term life insurance without Medical Exam. The difference with the Hancock policy is the rates. Most non medical term policies have rates that are 20% to 40% higher than comparable life policies that do require an exam. The John Hancock SmartProtect plan has both rates that are competitive and plans that are fully underwritten. Rates can go even lower if use the Vitality Program. It gives the insured a free Fitbit. You can be use the Fitbit to track your progress toward a healthy lifestyle. In fact, if you use the Vitality program you can lower your rates even further.

As an example:

A 46 year old male in good health can get $1,000,000 of SmartProtect term for 20 years for only $133 a month. If they use the Vitality program the rate can go as low as $86.75 a month. The rates with Vitality actually come out lower than the most competative life policies that do require an exam. The product is available to anyone age 20 to 60 and policies can be issued in about 3 days after submission of the application.

Please note that this policy does not require a medical exam but it does check on current health. In fact, this is not a guaranteed issue plan, some people will not be approved for a policy. Some companies may not accept people who have major health conditions. You can buy Term Life Insurance Without a Medical Exam. Contact our office if you want a quote or have any questions. Either by Phone- 203-796-5403 or email at Edward@croweandassociates.com

Click the links below for additional information on the policy:

John Hancock SmartProtect Term with Vitality pre qualification form